[ad_1]

Euro leads Sterling and Swiss Franc higher today, and stays firm so far. The common currency was apparently lifted by hawkish comments from ECB official over the weekend. Sterling shrugs off slightly worse than expected GDP and production data. Dollar and Yen are currently the weakest ones. Commodity currencies are mixed for now, with Canadian as the softer one.

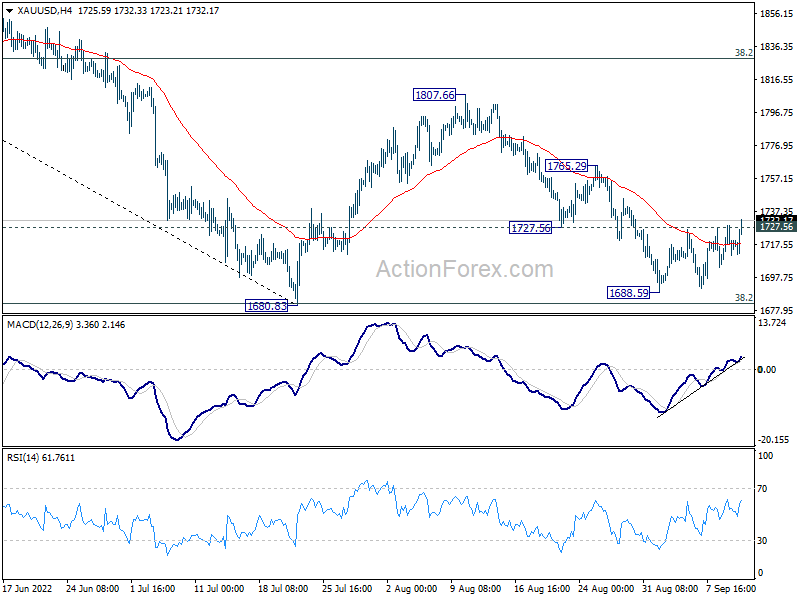

Technically, Gold’s break of 1727.56 support turned resistance suggests that fall from 1807.66 has completed at 1688.59. That came after defending 1680 long term support cluster. Rise from 1688.59 could either be the third leg of the pattern from 1680.83, or part of an up trend. In either case, further rise is now in favor to 1765.29 resistance first. Break will affirm near term bullishness and target 38.2% retracement of 2070.06 to 1680.83 at 1825.51.

In Europe, at the time of writing, FTSE is up 1.31%. DAX is up 1.65%. CAC is up 1.33%. Germany 10-year yield is down -0.0459 at 1.655. Earlier in Asia, Nikkei rose 1.16%. Japan 10-year JGB yield rose 0.0001 to 0.251. Singapore Strait Times rose 0.36%. Hong Kong and China were on Holiday.

UK GDP grew 0.2% mom in July, services up but production and construction down

UK GDP grew 0.2% mom in July, below expectation of 0.3% mom. Services grew 0.4% mom. Production dropped -0.3% mom. Construction also contracted -0.8% mom. For the three months to July, GDP was flat compared with the previous three months.

Also released, industrial production came in at -0.3% mom, 1.1% yoy, versus expectation of 0.4% mom, 2.0% yoy. Manufacturing production was at 0.1% mom, 1.1% yoy, versus expectation of 0.6% yoy. Goods trade deficit narrowed from GBP -22.8B to GBP -19.4B, versus expectation of GBP -23.2B.

NIESR: UK GDP to contract -0.1% in Q3, remains in recession

NIESR projects UK GDP to contract -0.1% in Q3, with growth slowing as inflation maintains its drag on consumer demand and confidence.

“GDP grew by 0.2 per cent in July following the large fall of 0.6 per cent in June. This was stronger than we had expected and was driven by a rise in services, particularly consumer-facing services, with production and construction continuing to fall. That said, GDP in the three months to July was flat relative to the previous three months and we think the UK economy remains in recession.” Stephen Millard Deputy Director for Macroeconomic Modelling and Forecasting, NIESR.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9991; (P) 1.0052; (R1) 1.0108; More…

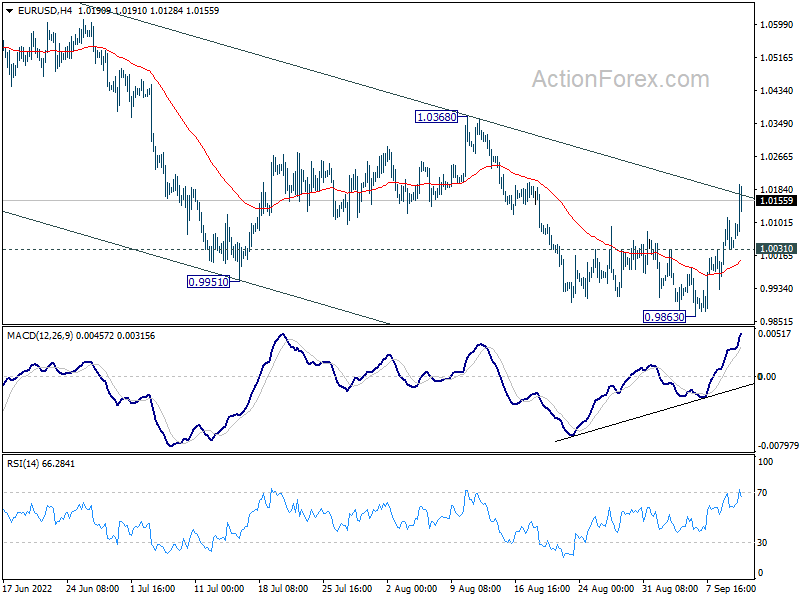

Intraday bias in EUR/USD remains on the upside as rebound from 0.9863 is extending. Sustained trading above 55 day EMA (now at 1.0169) raise the chance of larger trend reversal, and target 1.0368 resistance. On the downside, below 1.0031 minor support will turn bias back to the downside for retesting 0.9863 low.

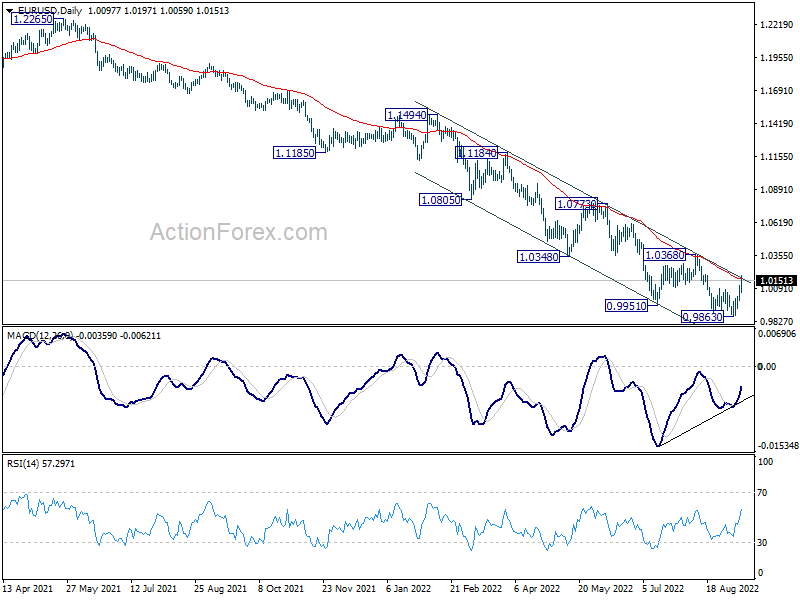

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0368 resistance holds, in case of strong rebound. However, firm break of 1.0368 will confirm medium term bottom at 0.9863 already.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Aug | 10.70% | 5.50% | ||

| 06:00 | GBP | GDP M/M Jul | 0.20% | 0.30% | -0.60% | |

| 06:00 | GBP | Industrial Production M/M Jul | -0.30% | 0.40% | -0.90% | |

| 06:00 | GBP | Industrial Production Y/Y Jul | 1.10% | 2.00% | 2.40% | |

| 06:00 | GBP | Manufacturing Production M/M Jul | 0.10% | 0.60% | -1.60% | |

| 06:00 | GBP | Manufacturing Production Y/Y Jul | 1.10% | 1.70% | 1.30% | |

| 06:00 | GBP | Index of Services 3M/3M Jul | -0.20% | -0.80% | -0.40% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | -19.4B | -23.2B | -22.8B | |

| 08:00 | EUR | Italy Industrial Output M/M Jul | 0.40% | 0.00% | -2.10% | -2.00% |

| 10:22 | GBP | NIESR GDP Estimate Aug | -0.30% | 0.00% |

[ad_2]

Source link